The global logistics landscape is witnessing a significant shift as the prolonged “freight recession” appears to be reaching its conclusion. Recent data from industry leaders suggests that the market is transitioning from a period of recovery into a more durable tightening cycle, driven by seasonal demand and structural capacity changes.

Điểm chính cần lưu ý

- Market Tightening: Freight rejection rates have reached 12.7%, a level not seen in several years, signaling a shift in pricing power toward carriers.

- Geopolitical Influence: Conflict in the Middle East continues to cause volatility in fuel markets, particularly affecting diesel prices near the Strait of Hormuz.

- Regulatory Disruptions: The upcoming CVSA International Roadcheck is expected to temporarily remove significant capacity from the road, potentially pushing rejection rates to 16-17%.

- Summer Peak Demand: June is projected to be a major month for freight, driven by the convergence of produce, construction, and industrial production cycles.

The End of the Freight Recession: A Market in Transition

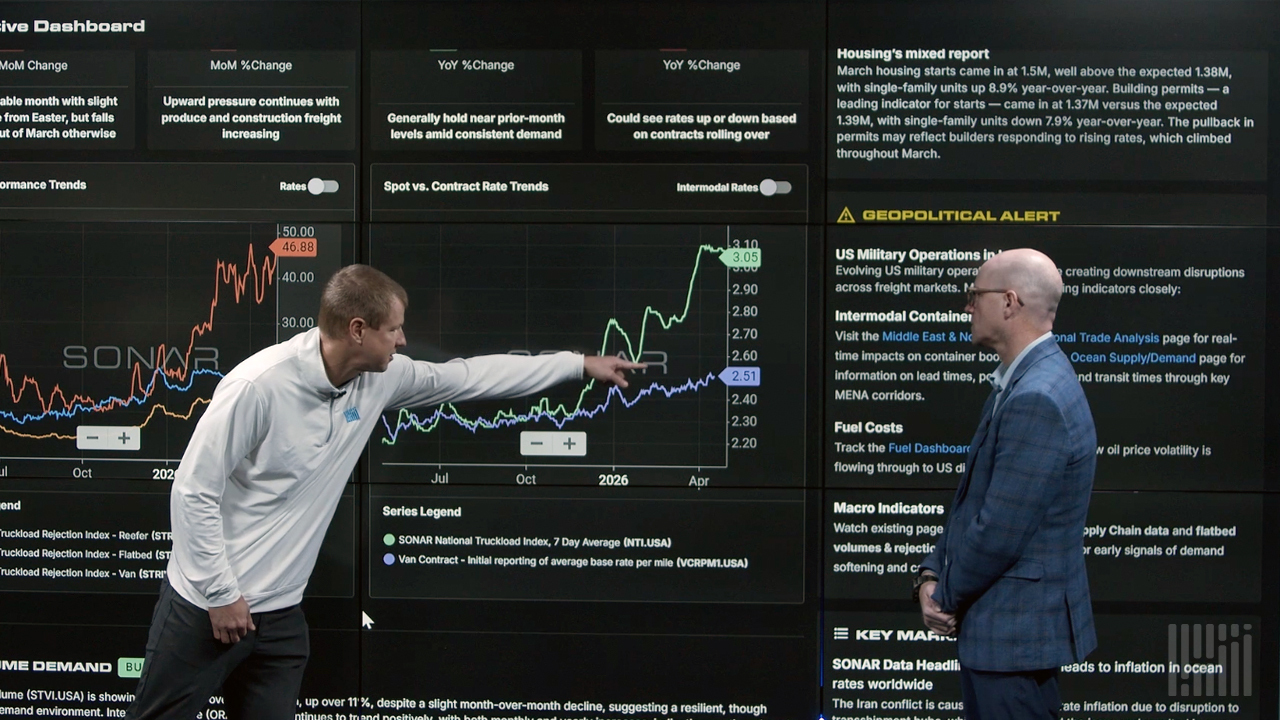

According to the latest State of Freight analysis, the market remains structurally tight despite seasonal softness in April. While March showed strong upward momentum, April has served as a “sideline” month—a typical seasonal trough before a massive acceleration expected in May and June. The most telling metric is the freight rejection rate, which currently sits at 12.7%. This indicates that carriers are increasingly in a position to decline low-paying loads, a hallmark of a tightening market.

Broader economic data is also indicating much stronger activity than previously expected. As a specialist in international logistics, M.T.L Worldwide Transport closely monitors these global capacity shifts to ensure our clients maintain supply chain continuity during market transitions. The resilience of the freight economy, even in the face of macro uncertainty, suggests that the bottom of the cycle has passed.

Geopolitical Factors and Fuel Price Volatility

Geopolitical disruptions, particularly involving Iran and the Strait of Hormuz, remain a primary driver of fuel price volatility. While high oil prices are a factor, analysts note that these costs are not necessarily sapping the strength of the broader economy. Instead, the market has seen significant spikes in retail diesel followed by corrections as military conflicts stabilize.

For logistics managers, the key takeaway is that fuel costs alone are not dictating pricing power. Instead, the underlying tightness in capacity is what enables carriers to adjust their rates. In the current environment, many carriers are successfully recovering fuel costs through rates, further stabilizing their operational margins as they head into the busier summer months.

Capacity Disruptions: The CVSA International Roadcheck

One of the most immediate concerns for supply chain planners is the upcoming CVSA International Roadcheck. This enforcement event is expected to see capacity come off the roads more than usual. Stricter enforcement and compliance scrutiny are already influencing driver behavior, with many choosing to stay off the road to avoid intensive inspections.

Because the market is already structurally tight with very little excess capacity, it has become much more sensitive to these types of disruptions. Experts predict that rejection rates could spike into the 16%–17% range during the enforcement period. Shippers should prepare for temporary delays and potential rate fluctuations during this window.

Preparing for the Summer Peak Demand Cycle

Looking ahead, the outlook for the summer shipping season is robust. Demand is building as we enter a much stronger seasonal cycle. June, in particular, is highlighted as the biggest month of the year due to the simultaneous peak of several sectors: produce, construction, and industrial production.

For procurement teams and e-commerce sellers, this means that the window for securing favorable capacity is narrowing. As industrial activity ramps up, the competition for available space will intensify. Understanding these global freight market update trends is essential for budgeting and inventory planning in the second half of the year.

Frequently Asked Questions

How will the CVSA International Roadcheck affect shipping capacity?

The CVSA International Roadcheck typically leads to a temporary reduction in available capacity as drivers avoid the road to bypass intensive inspections. In a tight market, this can cause freight rejection rates to spike to 16-17%, leading to short-term delays and higher spot market rates.

Why are freight rejection rates a key indicator for shippers?

Freight rejection rates measure the percentage of loads turned down by carriers. A rising rate, such as the current 12.7%, indicates that carriers have more options and higher pricing power, signaling the end of a freight recession and the start of a tightening market.

What impact do Middle East tensions have on freight costs?

Geopolitical tensions in the Middle East, particularly near the Strait of Hormuz, create volatility in diesel and oil prices. While this increases fuel surcharges, the broader impact is often managed by carriers through rate adjustments in a tightening capacity environment.